Simulateur Carnet d'Ordres & Liquidité [Sese] - Custom🔹 Indicator Name

Order Book & Liquidity Simulator - Custom

🔹 Concept and Functionality

This indicator is a technical analysis tool designed to visually simulate market depth (Order Book) and potential liquidity zones.

It is important to adhere to TradingView's transparency rules: This script does not access real Level 2 data (the actual exchange order book). Instead, it uses a deductive algorithm based on historical Price Action to estimate where Buy Limit (Bid) and Sell Limit (Ask) orders might be resting.

Methodology used by the script:

Pivot Detection: The indicator scans for significant Swing Highs and Swing Lows over a user-defined lookback period (Length).

Level Projection: These pivots are projected to the right as horizontal lines.

Red Lines (Ask): Represent potential resistance zones (sellers).

Blue Lines (Bid): Represent potential support zones (buyers).

Liquidity Management (Absorption): The script is dynamic. If the current price crosses a line, the indicator assumes the liquidity at that level has been consumed (orders filled). The line is then automatically deleted from the chart.

Density Profile (Right Side): Horizontal bars appear to the right of the current price. These approximate a "Time Price Opportunity" or Volume Profile, showing where the market has spent the most time recently.

🔹 User Manual (Settings)

Here is how to configure the inputs to match your trading style:

1. Detection Algorithm

Lookback Length (Candles): Determines the sensitivity of the pivots.

Low value (e.g., 10): Shows many lines (scalping/short term).

High value (e.g., 50): Shows only major structural levels (swing trading).

Volume Factor: (Technical note: In this specific code version, this variable is calculated but the lines are primarily drawn based on geometric pivots).

2. Visual Settings

Show Price Lines (Bid/Ask): Toggles the horizontal Support/Resistance lines on or off.

Show Volume Profile: Toggles the heatmap-style bars on the right side of the chart.

Extend Lines: If checked, untouched lines will extend to the right towards the current price bar.

3. Colors and Transparency Management

Customize the aesthetics to keep your chart clean:

Bid / Ask Colors: Choose your base colors (Default is Blue and Red).

Line Transparency (%): Crucial for chart visibility.

0% = Solid, bright colors.

80-90% = Very subtle, faint lines (recommended if you overlay this on other tools).

Text Size: Adjusts the size of the price labels ("BUY LIMIT" / "SELL LIMIT").

🔹 How to Read the Indicator

Rejections: Unbroken lines act as potential walls. Watch for price reaction when approaching a blue line (support) or red line (resistance).

Breakouts/Absorption: When a line disappears, it means the level has been breached. The market may then seek the next liquidity level (the next line).

Density (Right-side boxes): More opaque/visible boxes indicate a price zone "accepted" by the market (consolidation). Empty gaps suggest an imbalance where price might move through quickly.

⚠️ Disclaimer

This script is for educational and technical analysis purposes only. It is a simulation based on price history, not real-time order book data. Past performance is not indicative of future results. Trading involves risk.

在脚本中搜索"volume profile"

MRC Supply & Demand Zones by rnd🚀 MRC Supply & Demand Zones: Professional Reversal & Liquidity Detection

MRC Supply & Demand Zones is a premium hybrid trading tool combining two of the most powerful concepts in technical analysis: Mean Reversion and Volume Profile.

This indicator doesn’t just show arrows — it provides deep market context by defining dynamic volatility channels and hidden supply & demand zones based on real volume data from lower timeframes.

🔥 Key Features

1. MRC (Mean Reversion Channel)

At the core lies the SuperSmoother MA (SSMA) — a next-generation moving average that eliminates market noise significantly more effectively than standard SMAs or EMAs, while maintaining minimal lag.

Logic: Price always tends to return to its mean. The indicator constructs dynamic channels (Inner and Outer) around the SSMA based on volatility (True Range).

Signals:

Long (Buy): Price extends beyond the lower outer boundary (oversold) and closes back above it.

Short (Sell): Price extends beyond the upper outer boundary (overbought) and closes back below it.

2. Supply & Demand Zones

This is not just drawing levels based on simple highs and lows. The indicator utilizes Lower Timeframe (LTF) Data to construct a detailed volume profile inside the candles.

How it works: The algorithm scans history, identifies volume imbalances, and highlights zones where major players have shown significant interest.

Visualization: Automatically draws red (Supply) and blue (Demand) rectangles that act as price magnets and strong support/resistance levels.

⚙️ Settings Guide

🔹 Block: MRC Settings (Channel Settings)

Control signal sensitivity and channel width here.

Min Range %:

What: Sets the minimum channel width as a percentage of the current price.

Why: Prevents the channel from squeezing into a "thin line" during flat markets, filtering out false signals during low volatility.

Outer Multiplier:

Default: 1.9

Role: Defines the boundaries for "extreme" overbought/oversold conditions. Higher values result in fewer, but more accurate entry signals.

Inner Multiplier:

Default: 1.0

Role: Defines the boundaries of "normal" price oscillation. Often used as the first target for taking profits (Take Profit).

SSMA Length:

Default: 200

Role: The period of the main trend line. 200 is ideal for defining the long-term trend and the global "center" of price.

Source:

Default: hlc3 (High+Low+Close / 3).

Role: The price data used for calculations.

🔹 Block: Supply & Demand Zones

Controls the liquidity search algorithm.

Supply & Demand Zones (On/Off): Toggle the display of the rectangular zones.

Threshold %: Defines how "significant" the volume must be. Adjusts the filtering of weak zones.

Supply/Demand Zones Color: Select the color and opacity for seller and buyer zones.

Profile Lookback Range:

Fixed Range: Analyzes a fixed number of recent bars.

Visible Range: Analyzes only the bars currently visible on the screen.

Lookback Length: The depth of history (number of bars) for volume analysis (works in Fixed Range mode).

Profile Number of Rows: Profile resolution. Higher numbers result in more detailed and narrower zones.

🔔 Alert System

You will never miss an entry. The indicator includes built-in conditions for creating alerts:

Long Signal: Triggers on a green triangle (upward reversal from the lower boundary).

Short Signal: Triggers on a red triangle (downward reversal from the upper boundary).

💡 Why use this indicator?

This is a ready-made "all-in-one" trading strategy. You get the trend (SSMA), volatility (MRC), and liquidity levels (S&D) in one compact script. It is perfect for scalping and day trading on any asset (Crypto, Forex, Stocks).

Volume Area 80 Rule Pro - Adaptive RTHSummary in one paragraph

Adaptive value area 80 percent rule for index futures large cap equities liquid crypto and major FX on intraday timeframes. It focuses activity only when multiple context gates align. It is original because the classic prior day value area traverse is fused with a daily regime classifier that remaps the operating parameters in real time.

Scope and intent

• Markets. ES NQ SPY QQQ large cap equities BTC ETH major FX pairs and other liquid RTH instruments

• Timeframes. One minute to one hour with daily regime context

• Default demo used in the publication. ES1 on five minutes

• Purpose. Trade only the balanced days where the 80 percent traverse has edge while standing aside or tightening rules during trend or shock

Originality and usefulness

• Unique fusion. Prior day value area logic plus a rolling daily regime classifier using percentile ranks of realized volatility and ADX. The regime remaps hold time end of window stop buffer and value area coverage on each session

• Failure mode addressed. False starts during strong trend or shock sessions and weak traverses during quiet grind

• Testability. All gates are visible in Inputs and debug flags can be plotted so users can verify why a suggestion appears

• Portable yardstick. The regime uses ATR divided by close and ADX percent ranks which behave consistently across symbols

Method overview in plain language

The script builds the prior session profile during regular trading hours. At the first regular bar it freezes yesterday value area low value area high and point of control. It then evaluates the current session open location the first thirty minute volume rank the open gap rank and an opening drive test. In parallel a daily series classifies context into Calm Balance Trend or Shock from rolling percentile ranks of realized volatility and ADX. The classifier scales the rules. Calm uses longer holds and a slightly wider value area. Trend and Shock shorten the window reduce holds and enlarge stop buffers.

Base measures

• Range basis. True Range smoothed over a configurable length on both the daily and intraday series

• Return basis. Not required. ATR over close is the unit for regime strength

Components

• Prior Value Area Engine. Builds yesterday value area low value area high and point of control from a binned volume profile with automatic TPO fallback and minimum integrity guards

• Opening Location. Detects whether the session opens above the prior value area or below it

• Inside Hold Counter. Counts consecutive bars that hold inside the value area after a re entry

• Volume Gate. Percentile of the first thirty minutes volume over a rolling sample

• Gap Gate. Percentile rank of the regular session open gap over a rolling sample

• Drive Gate. Opening drive check using a multiple of intraday ATR

• Regime Classifier. Percentile ranks of daily ATR over close and daily ADX classify Calm Balance Trend Shock and remap parameters

• Session windows optional. Windows follow the chart exchange time

Fusion rule

Minimum satisfied gates approach. A re entry must hold inside the value area for a regime scaled number of bars while the volume gap and drive gates allow the setup. The regime simultaneously scales value area coverage end minute time stop and stop buffer.

Signal rule

• Long suggestion appears when price opens below yesterday value area then re enters and holds for the required bars while all gates allow the setup

• Short suggestion appears when price opens above yesterday value area then re enters and holds for the required bars while all gates allow the setup

• WAIT shows implicitly when any required gate is missing

• Exit labels mark target touch stop touch or a time based close

Inputs with guidance

Setup

• Signal timeframe. Uses the chart by default

• Session windows optional. Start and end minutes inside regular trading hours

• Invert direction is not used. The logic is symmetric

Logic

• Hold bars inside value area. Typical range 3 to 12. Raising it reduces trades and favors better traverses. Lowering it increases frequency and risk of false starts

• Earliest minute since RTH open and Latest minute since RTH open. Typical range 0 to 390. Reducing the latest minute cuts late session trades

• Time stop bars after entry. Typical range 6 to 30. Larger values give setups more room

Filters

• Value area coverage. Typical range 0.70 to 0.85. Higher coverage narrows the traverse but accepts fewer days

• Bin size in ticks. Typical range 1 to 8. Larger bins stabilize noisy profiles

• Stop buffer ticks beyond edge. Typical range 2 to 20. Larger buffers survive noise

• First thirty minute volume percentile. Typical range 0.30 to 0.70. Higher values require more active opens

• Gap filter percentile. Typical range 0.70 to 0.95. Lower values block more gap days

• Opening drive multiple and bars. Higher multiple or longer bars block strong directional opens

Adaptivity

• Lookback days for regime ranks. Typical 150 to 500

• Calm RV percentile. Typical 25 to 45

• Trend ADX percentile. Typical 55 to 75

• Shock RV percentile. Typical 75 to 90

• End minute ratio in Trend and Shock. Typical 0.5 to 0.8

• Hold and Time stop scales per regime. Use values near one to keep behavior close to static settings

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Shapes can move while a bar forms and settle on close

• Sessions use the chart exchange time

Honest limitations and failure modes

• Economic releases and thin liquidity can break the balance premise

• Gap heavy symbols may work better with stronger gap filters and a True Range focus

• Very quiet regimes reduce signal contrast. Consider longer windows or higher thresholds

Legal

Education and research only. Not investment advice. Test in simulation before any live use.

X rVPoCOverview

The rVPoC indicator isolates and displays the Volume Point of Control — the price level within a chosen lookback window that has accumulated the highest traded volume.

Unlike typical volume profiles that analyze an entire session or day, this version is designed for rolling intraday precision. It continually updates the VPoC using data from a lower “zoomed-in” timeframe (e.g., 1-minute) to refine accuracy, even when viewed on higher-timeframe charts.

How It Works

At its core, the indicator “zooms in” via Pine Script’s multi-timeframe engine:

Lower timeframe aggregation:

A secondary (zoomed) timeframe — by default 1-minute — is used to pull detailed OHLCV data through request.security().

Rolling window analysis:

The user-defined bars_per_current parameter determines how many of those lower-timeframe bars to include (e.g., 15 → a 15-minute rolling window).

Volume binning:

The high-to-low range of that window is divided into evenly spaced price bins (vp_price_levels). Each bin accumulates the volume of trades overlapping its range.

Point of Control selection:

The bin with the greatest accumulated volume is located, and its volume-weighted midpoint is plotted as the VPoC.

Visual output:

Discrete line-break markers are plotted for each bar, preventing the “connecting line” distortions common in continuous plots.

Use Case

This indicator is ideal for intraday traders who want to:

Track how the most active traded price shifts over time.

Identify short-term value zones forming within a 15-minute (or custom) rolling range.

Observe micro-structure behavior during developing sessions without committing to full volume profile tools.

Overlay a lightweight VPoC on top of other tools such as open-range or VWAP-based frameworks.

It is particularly effective on 1-minute and 5-minute charts, providing a granular yet efficient measure of volume concentration that updates bar-by-bar.

Summary

The VPoC indicator delivers a continuously updating micro-profile of where trading volume is most active within a chosen intraday window.

It’s designed to complement range, VWAP, and order-flow analysis by highlighting evolving value zones without visual clutter or session-anchoring logic.

Traders can interpret shifts in the VPoC as changes in short-term control — where buyers or sellers are concentrating their activity within the evolving price structure.

Smart MTF S/R Levels[BullByte]

Smart MTF S/R Levels

Introduction & Motivation

Support and Resistance (S/R) levels are the backbone of technical analysis. However, most traders face two major challenges:

Manual S/R Marking: Drawing S/R levels by hand is time-consuming, subjective, and often inconsistent.

Multi-Timeframe Blind Spots: Key S/R levels from higher or lower timeframes are often missed, leading to surprise reversals or missed opportunities.

Smart MTF S/R Levels was created to solve these problems. It is a fully automated, multi-timeframe, multi-method S/R detection and visualization tool, designed to give traders a complete, objective, and actionable view of the market’s most important price zones.

What Makes This Indicator Unique?

Multi-Timeframe Analysis: Simultaneously analyzes up to three user-selected timeframes, ensuring you never miss a critical S/R level from any timeframe.

Multi-Method Confluence: Integrates several respected S/R detection methods—Swings, Pivots, Fibonacci, Order Blocks, and Volume Profile—into a single, unified system.

Zone Clustering: Automatically merges nearby levels into “zones” to reduce clutter and highlight areas of true market consensus.

Confluence Scoring: Each zone is scored by the number of methods and timeframes in agreement, helping you instantly spot the most significant S/R areas.

Reaction Counting: Tracks how many times price has recently interacted with each zone, providing a real-world measure of its importance.

Customizable Dashboard: A real-time, on-chart table summarizes all key S/R zones, their origins, confluence, and proximity to price.

Smart Alerts: Get notified when price approaches high-confluence zones, so you never miss a critical trading opportunity.

Why Should a Trader Use This?

Objectivity: Removes subjectivity from S/R analysis by using algorithmic detection and clustering.

Efficiency: Saves hours of manual charting and reduces analysis fatigue.

Comprehensiveness: Ensures you are always aware of the most relevant S/R zones, regardless of your trading timeframe.

Actionability: The dashboard and alerts make it easy to act on the most important levels, improving trade timing and risk management.

Adaptability: Works for all asset classes (stocks, forex, crypto, futures) and all trading styles (scalping, swing, position).

The Gap This Indicator Fills

Most S/R indicators focus on a single method or timeframe, leading to incomplete analysis. Manual S/R marking is error-prone and inconsistent. This indicator fills the gap by:

Automating S/R detection across multiple timeframes and methods

Objectively scoring and ranking zones by confluence and reaction

Presenting all this information in a clear, actionable dashboard

How Does It Work? (Technical Logic)

1. Level Detection

For each selected timeframe, the script detects S/R levels using:

SW (Swing High/Low): Recent price pivots where reversals occurred.

Pivot: Classic floor trader pivots (P, S1, R1).

Fib (Fibonacci): Key retracement levels (0.236, 0.382, 0.5, 0.618, 0.786) over the last 50 bars.

Bull OB / Bear OB: Institutional price zones based on bullish/bearish engulfing patterns.

VWAP / POC: Volume Weighted Average Price and Point of Control over the last 50 bars.

2. Level Clustering

Levels within a user-defined % distance are merged into a single “zone.”

Each zone records which methods and timeframes contributed to it.

3. Confluence & Reaction Scoring

Confluence: The number of unique methods/timeframes in agreement for a zone.

Reactions: The number of times price has touched or reversed at the zone in the recent past (user-defined lookback).

4. Filtering & Sorting

Only zones within a user-defined % of the current price are shown (to focus on actionable areas).

Zones can be sorted by confluence, reaction count, or proximity to price.

5. Visualization

Zones: Shaded boxes on the chart (green for support, red for resistance, blue for mixed).

Lines: Mark the exact level of each zone.

Labels: Show level, methods by timeframe (e.g., 15m (3 SW), 30m (1 VWAP)), and (if applicable) Fibonacci ratios.

Dashboard Table: Lists all nearby zones with full details.

6. Alerts

Optional alerts trigger when price approaches a zone with confluence above a user-set threshold.

Inputs & Customization (Explained for All Users)

Show Timeframe 1/2/3: Enable/disable analysis for each timeframe (e.g., 15m, 30m, 1h).

Show Swings/Pivots/Fibonacci/Order Blocks/Volume Profile: Select which S/R methods to include.

Show levels within X% of price: Only display zones near the current price (default: 3%).

How many swing highs/lows to show: Number of recent swings to include (default: 3).

Cluster levels within X%: Merge levels close together into a single zone (default: 0.25%).

Show Top N Zones: Limit the number of zones displayed (default: 8).

Bars to check for reactions: How far back to count price reactions (default: 100).

Sort Zones By: Choose how to rank zones in the dashboard (Confluence, Reactions, Distance).

Alert if Confluence >=: Set the minimum confluence score for alerts (default: 3).

Zone Box Width/Line Length/Label Offset: Control the appearance of zones and labels.

Dashboard Size/Location: Customize the dashboard table.

How to Read the Output

Shaded Boxes: Represent S/R zones. The color indicates type (green = support, red = resistance, blue = mixed).

Lines: Mark the precise level of each zone.

Labels: Show the level, methods by timeframe (e.g., 15m (3 SW), 30m (1 VWAP)), and (if applicable) Fibonacci ratios.

Dashboard Table: Columns include:

Level: Price of the zone

Methods (by TF): Which S/R methods and how many, per timeframe (see abbreviation key below)

Type: Support, Resistance, or Mixed

Confl.: Confluence score (higher = more significant)

React.: Number of recent price reactions

Dist %: Distance from current price (in %)

Abbreviations Used

SW = Swing High/Low (recent price pivots where reversals occurred)

Fib = Fibonacci Level (key retracement levels such as 0.236, 0.382, 0.5, 0.618, 0.786)

VWAP = Volume Weighted Average Price (price level weighted by volume)

POC = Point of Control (price level with the highest traded volume)

Bull OB = Bullish Order Block (institutional support zone from bullish price action)

Bear OB = Bearish Order Block (institutional resistance zone from bearish price action)

Pivot = Pivot Point (classic floor trader pivots: P, S1, R1)

These abbreviations appear in the dashboard and chart labels for clarity.

Example: How to Read the Dashboard and Labels (from the chart above)

Suppose you are trading BTCUSDT on a 15-minute chart. The dashboard at the top right shows several S/R zones, each with a breakdown of which timeframes and methods contributed to their detection:

Resistance zone at 119257.11:

The dashboard shows:

5m (1 SW), 15m (2 SW), 1h (3 SW)

This means the level 119257.11 was identified as a resistance zone by one swing high (SW) on the 5-minute timeframe, two swing highs on the 15-minute timeframe, and three swing highs on the 1-hour timeframe. The confluence score is 6 (total number of method/timeframe hits), and there has been 1 recent price reaction at this level. This suggests 119257.11 is a strong resistance zone, confirmed by multiple swing highs across all selected timeframes.

Mixed zone at 118767.97:

The dashboard shows:

5m (2 SW), 15m (2 SW)

This means the level 118767.97 was identified by two swing points on both the 5-minute and 15-minute timeframes. The confluence score is 4, and there have been 19 recent price reactions at this level, indicating it is a highly reactive zone.

Support zone at 117411.35:

The dashboard shows:

5m (2 SW), 1h (2 SW)

This means the level 117411.35 was identified as a support zone by two swing lows on the 5-minute timeframe and two swing lows on the 1-hour timeframe. The confluence score is 4, and there have been 2 recent price reactions at this level.

Mixed zone at 118291.45:

The dashboard shows:

15m (1 SW, 1 VWAP), 5m (1 VWAP), 1h (1 VWAP)

This means the level 118291.45 was identified by a swing and VWAP on the 15-minute timeframe, and by VWAP on both the 5-minute and 1-hour timeframes. The confluence score is 4, and there have been 12 recent price reactions at this level.

Support zone at 117103.10:

The dashboard shows:

15m (1 SW), 1h (1 SW)

This means the level 117103.10 was identified by a single swing low on both the 15-minute and 1-hour timeframes. The confluence score is 2, and there have been no recent price reactions at this level.

Resistance zone at 117899.33:

The dashboard shows:

5m (1 SW)

This means the level 117899.33 was identified by a single swing high on the 5-minute timeframe. The confluence score is 1, and there have been no recent price reactions at this level.

How to use this:

Zones with higher confluence (more methods and timeframes in agreement) and more recent reactions are generally more significant. For example, the resistance at 119257.11 is much stronger than the resistance at 117899.33, and the mixed zone at 118767.97 has shown the most recent price reactions, making it a key area to watch for potential reversals or breakouts.

Tip:

“SW” stands for Swing High/Low, and “VWAP” stands for Volume Weighted Average Price.

The format 15m (2 SW) means two swing points were detected on the 15-minute timeframe.

Best Practices & Recommendations

Use with Other Tools: This indicator is most powerful when combined with your own price action analysis and risk management.

Adjust Settings: Experiment with timeframes, clustering, and methods to suit your trading style and the asset’s volatility.

Watch for High Confluence: Zones with higher confluence and more reactions are generally more significant.

Limitations

No Future Prediction: The indicator does not predict future price movement; it highlights areas where price is statistically more likely to react.

Not a Standalone System: Should be used as part of a broader trading plan.

Historical Data: Reaction counts are based on historical price action and may not always repeat.

Disclaimer

This indicator is a technical analysis tool and does not constitute financial advice or a recommendation to buy or sell any asset. Trading involves risk, and past performance is not indicative of future results. Always use proper risk management and consult a financial advisor if needed.

Order Flow Delta Matrix Pro @MaxMaserati 2.0Order Flow Delta Matrix Pro @MaxMaserati 2.0

Institutional-level order flow analysis

This advanced indicator displays institutional order flow data in an easy-to-read time-series matrix, revealing hidden buying and selling pressure that drives price movements.

KEY FEATURES

🔥 REAL-TIME DELTA TRACKING

- Delta Row: Net buying vs selling pressure per time period

- Live Countdown: Shows exact time remaining until next candle close

- Extended historical view for pattern recognition

CUSTOMIZABLE ROWS (Toggle On/Off)

- Max Delta: Highest buying pressure spikes (accumulation zones)

- *Min Delta: Lowest selling pressure spikes (distribution zones)

- Cumulative Delta: Running total showing institutional bias

- Delta/Volume Ratio: Quality of directional flow vs total volume

- Session Delta: Net flow since session start

- Volume: Raw transaction volume with high-volume highlighting

ADVANCED CONTROLS

- Time Direction: View oldest→newest OR newest→oldest

- 12/24 Hour Format: Choose your preferred time display

- Current Time Highlighting: Blue highlight on active time period

- Full Color Customization: Adapt to any chart theme

- Smart Sensitivity: Low/Normal/High modes for different markets

🎓 HOW TO USE IT

🟢 BULLISH SIGNALS

- Positive Delta Spikes: Look for green +500K+ delta values

- Rising Cumulative Delta: Upward trending cumulative line = institutional accumulation

- High Max Delta: Strong buying pressure at support levels

🔴 BEARISH SIGNALS

- Negative Delta Spikes: Look for red -500K+ delta values

- Falling Cumulative Delta: Downward trending cumulative = institutional distribution

- High Min Delta: Strong selling pressure at resistance levels

PRO TECHNIQUES

-Divergence Analysis: Price goes up but cumulative delta goes down = potential reversal

- Volume Confirmation: High delta + high volume = strong institutional conviction

- Session Bias: Positive session delta = bullish bias, negative = bearish bias

BEST USED FOR

- Scalping: 1-5 minute timeframes for quick institutional flow detection

- Day Trading: 15-60 minute timeframes for session bias and reversal spots

- Volume Profile: Combine with volume profile for complete order flow picture

- Futures Trading: Excellent for ES, NQ, crude oil, forex majors

PRO TIPS

1. Watch for Delta Divergences - Most reliable reversal signal

2. High Volume + High Delta = Institutional activity

3. Session Delta Direction = Overall market bias

4. Blue highlighted column= Current live data

5. Use with Support/Resistance for entry/exit timing

IMPORTANT NOTES

- Works on ALL timeframes and ALL markets

- Real-time updates for live trading decisions

- Historical data available for backtesting strategies

- No repainting - all signals are final and reliable

The matrix format makes complex data easy to interpret, giving a significant edge in understanding market dynamics and smart money order timing.

Volume Footprint POC for Every CandleCalculating and plotting the Point of Control (POC) for every candle on a volume footprint chart can provide valuable insights for traders. Here are some interpretations and uses of this information:

1. Identify Key Price Levels

Highest Traded Volume: The POC represents the price level with the highest traded volume for each candle. This level often acts as a significant support or resistance level.

Confluence Zones: When multiple POCs align at similar price levels over several candles, it indicates strong support or resistance zones.

2. Gauge Market Sentiment

Buyer and Seller Activity: High volume at certain price levels can indicate where buyers and sellers are most active. A rising POC suggests stronger buying activity, while a falling POC suggests stronger selling activity.

Volume Profile: Analyzing the volume profile helps in understanding the distribution of traded volume across different price levels, providing insights into market sentiment and potential reversals.

3. Spot Trends and Reversals

Trend Continuation: Consistent upward or downward shifts in POC levels can indicate a trend continuation. Traders can use this information to stay in trending positions.

Reversal Signals: A sudden change in the POC direction may signal a potential reversal. This can be used to take profits or enter new positions.

4. Intraday Trading Strategies

Short-Term Trading: Intraday traders can use the POC to make informed decisions on entry and exit points. For example, buying near the POC during an uptrend or selling near the POC during a downtrend.

Scalping Opportunities: High-frequency traders can use shifts in the POC to scalp small profits from price movements around these key levels.

5. Volume-Based Indicators

Confirmation of Other Indicators: The POC can be used in conjunction with other technical indicators (e.g., moving averages, RSI) to confirm signals and improve trading accuracy.

Support and Resistance: Combining the POC with traditional support and resistance levels can provide a more comprehensive view of the market dynamics.

In summary, the Point of Control (POC) is a valuable tool for traders to understand market behavior, identify key levels, and make more informed trading decisions. If you have specific questions or need further details on how to use this information in your trading strategy, feel free to ask! 😊

Hybrid Profile [DW]This is an experimental study inspired by J. Peter Steidlmayer's Market Profile tool with an alternative set of calculations for analyzing price action and distribution over a defined interval.

This tool is geared toward finding price reactive points for better entry and exit positions.

In this script, price range over a user defined interval (up to 4000 bars) is divided into 50 sections, then TPOs are counted for each section to generate the distribution histogram. Histogram lines are calculated in real time, and recalculate on each new bar.

Areas of significance are displayed as purple lines in the histogram, making it incredibly simple to identify levels that price will likely react to. The significance sensitivity can be manually adjusted for desired output.

Rather than using POC, I created a series of proprietary calculations to generate what I call the Point Of Focus (POF). This line is similar to POC, but does not always follow the highest count in the distribution.

The POF is designed to experience less whipsaws than POC, which makes trading using the POF much simpler since its value is more consistent. On historical data, price has shown to either revert to or launch from the POF rather frequently.

Unlike a conventional Market Profile, this profile doesn't have a "value area". Instead it has a Mean Value Zone, which is calculated using a series of custom VWAP calculations. The output is similar to VA, but much smoother.

This script has a built in tick volume substitution for charts with no real volume data, making all elements of the script compatible with any cryptocurrency, stock, currency pair, or index you want to analyze.

A bar color scheme is included within this script which can be used to help determine dominant trend and local extremes of the interval.

This tool is not necessarily better or worse than the classic Market Profile, nor is it a replacement for Volume Profile.

However, this is a powerful alternative that can both simplify and improve your technical analysis.

AMT Structure: 80% Traverse, PD Levels & nPOCsHere is a clean, professional description formatted for the TradingView description box. It highlights the methodology (AMT/80% Rule), the specific features, and the credits.

Title: AMT Structure: 80% Traverse, PD Levels & nPOCs

Description:

This indicator is a comprehensive toolkit designed for futures traders utilizing Auction Market Theory (AMT) and Volume Profile strategies. It consolidates multiple scripts into a single, unified overlay to declutter your chart while providing essential structural references for the 80% Traverse setup, intraday context, and longer-term auction targets.

Key Features:

1. 80% Rule / Traverse Setup (Chart Champions Logic)

Automated RTH Open Detection: Hardcoded to the 08:30 AM CT Open to ensure accuracy for US Futures (ES/NQ) regardless of your chart's timezone settings.

Value Area Logic: Automatically calculates the Previous Day's Value Area High (VAH), Value Area Low (VAL), and Point of Control (POC).

Setup Detection: If the market opens outside of the previous day's value, the script highlights the Value Area in color (default: Purple), signaling that an 80% traverse (filling the value area) is structurally possible if price re-enters value.

Background Fill: Optional shading between VAH and VAL to clearly visualize the "playing field" for the traverse.

2. Auction Market Theory (AMT) Premarket Levels

Overnight High/Low: Automatically captures the highest and lowest prices traded during the overnight session (17:00 - 08:30 CT).

Breakout Alerts: Includes logic to detect and alert when these overnight levels are broken during the RTH session.

Auto-Cleanup: Lines can be set to auto-delete after a specified time (default: 60 mins into the session) to keep the chart clean after the Initial Balance (IB) period.

3. Structural Reference Levels

Previous Day Levels: Plots Previous Day High, Low, and Equilibrium (Midpoint) as standard reference lines.

Initial Balance (IB): Option to display the First Hour High and Low (08:30 - 09:30 CT) to assess day type (Neutral, Trend, Normal Variation, etc.).

RTH VWAP: An anchored VWAP that resets specifically at the RTH Open (08:30 CT), distinct from the standard 24-hour VWAP.

4. Naked Points of Control (nPOCs)

Multi-Timeframe Tracking: Tracks and plots Naked POCs for Daily, Weekly, and Monthly profiles.

Auto-Cleanup: Lines automatically delete themselves the moment price touches them, ensuring you only see untested levels.

Customization: Toggle each timeframe on/off individually.

Settings & Customization:

Global Offset: Move all text labels to the right with a single setting to prevent price action from obscuring text.

8:30 Open Offset: Independent offset for the Open label to distinguish it from other opening references.

Smart Coloring: Text labels automatically match their corresponding line colors for easy identification.

Modular Toggles: Every section (AMT, VWAP, PD Levels, CCV, nPOCs) can be turned on or off individually to suit your specific trading plan.

Usage: This tool is specifically tuned for ES and NQ futures trading but can be adapted for other instruments. It replaces the need for separate indicators for Overnight Highs/Lows, Previous Day Levels, and Volume Profile targeting.

Multy Dynamic POCThis script displays up to 4 independent Point of Control (POC) levels based on volume profile logic.

📌 Each POC can be configured individually:

Period options: Daily (D), Weekly (W), Monthly (M), or BARS (rolling bar window).

Dynamic recalculation when the period changes (e.g., new day/week/month or custom bar count).

Price-anchored lines for each POC level that scale correctly with the chart.

Customizable line color and thickness.

🔍 How it works:

For each active POC line, the script builds a simple volume distribution based on the candle’s average price (hl2) and volume.

The price range is split into 100 buckets. The one with the highest accumulated volume is selected as the Point of Control (POC).

In BARS mode, POC is recalculated every N bars. In D/W/M modes, it resets exactly at the beginning of a new period (according to TradingView’s time() function).

✅ Useful for:

Traders applying volume profile analysis without needing the full built-in volume profile tool.

Spotting dynamic high-volume zones in trends or ranges.

Strategy development or confirmation around high-interest price levels.

_______________________________________________________________________________

Данный индикатор отображает до 4 независимых уровней Point of Control (POC), рассчитанных по объёмам.

📌 Каждый POC можно настраивать отдельно:

Периоды: День (D), Неделя (W), Месяц (M) или BARS (скользящее окно по количеству баров).

Автоматический пересчёт при смене периода (например, новый день, неделя или месяц).

Линии POC привязаны к цене и масштабируются вместе с графиком.

Настраиваемый цвет и толщина линий.

🔍 Как работает:

Для каждой активной линии POC создаётся объёмное распределение: берется средняя цена свечи (hl2) и объем.

Диапазон цен делится на 100 уровней. Тот, где накоплено больше всего объёма, и есть POC.

В режиме BARS уровень пересчитывается каждые N баров. В режимах D/W/M — строго в начале нового периода.

✅ Подходит для:

Трейдеров, использующих объёмный анализ, но не имеющих платной подписки на Volume Profile.

Поиска уровней интереса и подтверждения сигналов.

Разработки стратегий с опорой на объём.

Period Value ZonesPeriod Value Zones is designed to help traders understand where current value is being found by splitting the day into 3 key periods based on common reversal times recognized for intraday trading.

By splitting the day into 3 periods, we can more efficiently determine where short-term value lies by using only the data we consider relevant during these periods of time.

> Overview

This indicator is recommended for low timeframe trading during the New York RTH Session.

By only trading within this session, we can ensure that volume and volatility remain fairly consistent.

Within each Period, you will find on the chart:

Value Area Points from Previous period (Value High(VAH)/Value Low(VAL)/Point of Control(POC))

Volume Weighted Average Price (VWAP) Cloud, based on High and Low values during the period.

Value Zone based Potential Reversal Zones.

Additional Displays:

Potential Reversal Detection Signals with Invalidation Levels

Forward Plotted Key Market times.

> Components

• Value Area Points

VAH/VAL/POC are important volume profile points which display where the market has previously held value.

We use these specific levels as support and resistance to confirm direction by monitoring interactions between price and these important levels.

The VAH and VAL lines change colors based on price's interaction with them to confirm whether that level should be regarded as support or resistance.

• VWAP Cloud

VWAP is a common metric used to determine the strength of a trend, and provides a point to look for re-bid & re-offer.

When price breaks out of our Fixed Value zone, VWAP helps us determine further direction.

Also included is VWAP deviation bands, for traders who would prefer to view the standard deviation away from this cloud as well.

• Value Reversal Zones

These Zones are calculated based on extensions of the Period Value Zone.

While in a balanced market, these zones have been shown to provide potential reversal opportunities.

• Potential Reversal Signals

These signals are based on an advanced method for confirming a higher-low or lower-high to reasonably create a signal that is not very laggy but also rooted in sound logic.

While helpful, These are NOT buy or sell signals, and you should always use further analysis to decide the next steps to take.

When a signal appears, an associated invalidation level is also displayed, if this level is crossed the associated signal is no longer considered relevant.

• Key Market Times

These are important times within the day that normally produce volatility caused by daily market catalysts.

Each key time is forward plotted 1 hour before it occurs to provide a clear heads up for potential opportunity.

Opening Fuel: Known for having an increase in Volume after the formation of the 15min Opening Range.

1st Reversal: Common Area for seeing initial large positioning effecting the market, often causing reversals.

Initial Balance Close: End of the first hour, a common positioning tool for futures traders.

2nd Reversal: Positioning is typically reactionary to IB Close, alongside Euro Traders Exiting Positions.

Euro Close: Close of Europe Session, a common positioning tool for futures traders.

Lunch: Usually Low Volume, traders are often out to lunch.

Lunch End: Volume tends to re-enter, as traders come back from lunch.

1st Reversal: New Hour, common area to see large position re-enter the market.

Bonds Close: Bonds markets close, Equities reacting to close of the bond market.

1st MOC: Initial Market on Close orders are places, market reaction is normally expected off of MOC positioning.

MOC Close: As MOC orders are reported, volatility is likely found within the market.

> Methodology

This indicator can be used with the same principles as trading balanced volume profiles.

Rule 1: Unless the price breaks and holds Value High or Value Low, we should expect buyers and sellers to maintain the current balance.

Rule 2: If we break and push away from the Period Value High, we should treat that level as supportive on retest unless we look back below and sellers defend on retest.

Rule 3: If we break and push away from the Period Value Low, we should treat that level as resistance on retest unless we look back above and buyers defend on retest.

Rule 4: If we recover Value Low, and it becomes supportive, we look for our Period POC and Period Value High as our targets above.

Rule 5: If we fail to hold Period Value High, and it becomes resistance, we look for our Period POC and Period Value Low as targets below.

Balance in the context of this indicator is considered as the area between Period Value High and Period Value Low

Acceptance outside of balance in the context of this indicator is considered as Period Value Low or High, becoming supportive or resistance.

> Examples

Theoretical Example:

In the bullish example below, price holds VWAP and makes POC supportive, showing interest from buyers pushing to Value High.

Real-World Example:

Below is an example of the same setup as the theoretical example, taking place on a real futures chart.

By utilizing these rules, we can look for opportunities at these levels and have a plan for how we should be interacting with them.

This will help us determine likely targets and risk-off levels that are based on volume and current "value" from participants.

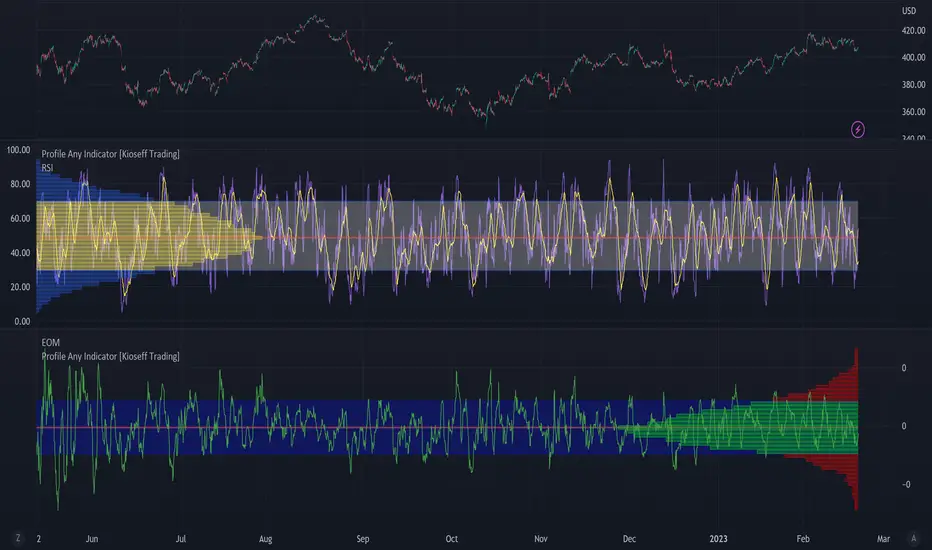

Profile Any Indicator [Kioseff Trading]Create a visible-range profile for almost any indicator!

Hello!

This script "Profile Any Indicator" allows you to create a visible-range profile for *almost* any indicator hosted on TradingView.

Therefore, the only requirement:

1. Indicator must have a retrievable plot value.

Should your indicator have a retrievable plot value (most indicators do), you can use this script to create a visible-range profile of its values!

Consequently, the profile's always oriented to the left-most or right-most side of your chart - updating as you scroll left or right.

The image above shows me using the indicator to create a profile for MACD. I am largely zoomed out and the profile has adjusted to chart orientation.

Let's zoom in and see what happens!

Voila!

The indicator adjusted to my chart positioning and created a new visible-range profile! No manual adjustments are required (:

Instructions

1. Load the indicator you'd like to profile on the chart.

The image above shows me applying the OBV indicator to the chart. Additionally, the "Profile Any Indicator" script is also loaded on the chart, instructing me to add an indicator to its settings.

2. From the settings for "Profile Any indicator", locate the "Indicator" setting and select the indicator you would like to profile.

The image above shows me selecting the OBV indicator in the settings for "Profile Any Indicator".

Once steps 1 and 2 are complete you'll have a visible-range profile for the selected indicator on your chart!

The image above shows the completion of the process.

3. Merge the indicator pane or select to plot the selected indicator in the current pane.

From here, you can select to plot the value of the selected indicator in the current pane or merge the selected indicator's pane (which must stay on the chart) with the pane designated to the "Profile Any Indicator" script.

The image above shows the two panes merged.

The image above shows the two panes separate. Alternatively, in the settings for "Profile Any Indicator", I selected to plot OBV in its pane.

You can select to populate the visible-range profile on the right of the chart!

Additionally, you can modify the POC line, value area %, and, essentially, any parameter you'd find for a volume-profile-like indicator!

Thanks for checking this out (:

Statistcal Daily Profile & Ranges# Statistical Daily Profile & Ranges - TradingView Publication Guide

## Overview

The **Statistical Daily Profile & Ranges** indicator is a comprehensive tool designed to analyze intraday session behavior and daily range characteristics. It combines Average Daily Range (ADR) projection levels with detailed session-by-session statistics and probability-based trading insights derived from historical price action patterns.

## What This Indicator Does

This indicator provides traders with three core analytical components:

1. **ADR Projection Levels** - Dynamic support/resistance levels based on historical daily ranges

2. **Session Range Analysis** - Visual boxes and statistical breakdowns for four key trading sessions

3. **Dynamic Probability Display** - Real-time probability statistics based on overnight session relationships

## How It Works

### Average Daily Range (ADR) Calculation

The indicator calculates the average daily range over a user-defined lookback period (default: 10 days) and projects this range from each day's opening price. This creates two key levels:

- **ADR High**: Opening price + average daily range

- **ADR Low**: Opening price - average daily range

- **ADR Median**: The opening price (middle of the projected range)

These levels are recalculated at the start of each trading day and extend forward, providing dynamic support and resistance zones based on recent volatility characteristics.

### Session Tracking & Statistics

The indicator monitors four distinct trading sessions (times in Eastern Time):

1. **Asia Session** (8:00 PM - 2:00 AM)

2. **London Session** (2:00 AM - 8:00 AM)

3. **NY Open** (8:00 AM - 9:00 AM)

4. **NY Initial Balance** (9:30 AM - 10:30 AM)

For each session, the indicator:

- Draws a colored box showing the session's high-to-low range

- Tracks the opening price, high, and low

- Stores historical data for statistical analysis

- Calculates average ranges by day of week (Monday through Friday)

The session statistics are displayed in a customizable table showing average point ranges for each session across different weekdays, helping traders identify which sessions and days typically produce the most movement.

### Dynamic Probability System

The indicator analyzes the relationship between the Asia and London sessions to determine the current market setup. After the London session closes, it automatically detects one of four possible conditions:

**1. London Engulfs Asia**

- London session breaks both above Asia's high AND below Asia's low

- This indicates strong momentum during the European session

- Most common occurrence pattern

**2. Asia Engulfs London**

- Asia session range completely contains the London session range

- Indicates consolidation during London hours

- Relatively rare pattern (occurs approximately 5.36% of the time)

**3. London Partially Engulfs Upwards**

- London breaks above Asia's high but stays above Asia's low

- Suggests bullish momentum continuation from Asia into London

**4. London Partially Engulfs Downwards**

- London breaks below Asia's low but stays below Asia's high

- Suggests bearish momentum continuation from Asia into London

Once a condition is detected, the indicator displays a probability table showing historically observed outcomes for that specific setup, including:

- Probability of NY session taking out key levels (Asia high/low, London high/low)

- Probability of NY session engulfing the entire overnight range

- Directional bias for NY Cash session (9:30 AM - 4:00 PM)

## How to Use This Indicator

### Initial Setup

1. Add the indicator to your chart (works on any intraday timeframe below Daily)

2. Adjust the **ADR Days** setting (default: 10) to control the lookback period for range calculation

3. Adjust the **Session Lookback Days** setting (default: 50) to determine how much historical data feeds the statistics tables

### Reading the ADR Levels

- Use the **ADR High** and **ADR Low** lines as potential profit targets or areas where price may encounter resistance

- The **ADR Median** line represents the opening price and can act as a pivot point for intraday directional bias

- If price reaches the ADR High early in the session, it suggests strong bullish momentum; conversely for ADR Low

- These levels adapt daily based on recent volatility, making them more responsive than static levels

### Interpreting Session Boxes

- **Session boxes** visually highlight when each trading session is active and its price range

- Larger boxes indicate higher volatility during that session

- Compare current session ranges to the statistical averages shown in the table

- Sessions that are unusually quiet or active relative to historical averages may signal compression or expansion

### Using the Session Statistics Table

- The table shows average point ranges for each session broken down by weekday

- Identify which sessions typically produce the most movement on specific days

- For example, if London on Thursdays averages 40 points while Mondays average 25 points, you can adjust position sizing or expectations accordingly

- The **Total** column shows the overall average across all days

- Sample sizes (shown in brackets if enabled) indicate data reliability

### Trading with the Probability Table

The probability table updates dynamically after the London session closes and shows statistically probable outcomes based on 12 years of NQ futures data.

**Important Limitations:**

- **These probabilities are derived from NQ (Nasdaq E-mini futures) data only**

- **Do NOT apply these probability statistics to other instruments** (ES, stocks, forex, etc.)

- The probabilities represent historical frequencies, not guarantees

- Always combine with your own analysis, risk management, and market context

**How to Apply the Probabilities:**

When **London Engulfs Asia**:

- Watch for NY session to take out London's extremes (72.33% probability for high, 71.12% for low)

- Slight bullish bias in NY Cash session (54.80% vs 45.20%)

- Lower probability of complete overnight engulfment (44.13%)

When **Asia Engulfs London** (rare - 5.36% occurrence):

- Higher probability NY takes Asia's high (75.86%)

- Moderately high probability NY takes Asia's low (65.52%)

- Slight increase in bullish bias (58.42% vs 41.58%)

- Recognize this as an unusual setup

When **London Partially Engulfs Upwards**:

- Very high probability NY takes London high (81.51%)

- Strong probability NY takes London low (64.45%)

- Moderate probability NY takes Asian low (53.16%)

- Slight bullish bias (55.52%)

When **London Partially Engulfs Downwards**:

- Very high probability NY takes London low (75.29%)

- Strong probability NY takes London high (68.80%)

- Moderate probability NY takes Asian high (56.44%)

- Slight bullish bias maintained (52.99%)

### Practical Trading Applications

**Scenario 1: Range Projection**

If the ADR is 500 points and the market opens at 25,000:

- ADR High: 25,500 (potential resistance/target)

- ADR Low: 24,500 (potential support/target)

- Monitor how price interacts with these levels throughout the day

**Scenario 2: Session-Based Trading**

Using the statistics table, you notice London on Wednesdays averages 35 points. During a Wednesday London session:

- If London has already moved 30 points, the session may be exhausting its typical range

- If London has only moved 15 points with an hour remaining, there may be expansion potential

- Adjust stop losses and targets based on typical session behavior

**Scenario 3: Probability-Based Setup**

It's 8:05 AM ET and the indicator shows "London Partially Engulfs Upwards":

- You now know there's an 81.51% historical probability NY will take out London's high

- There's a 53.16% probability NY will reach down to Asia's low

- The NY Cash session has a slight bullish bias (55.52%)

- Consider this alongside your technical analysis for directional bias and level targeting

## Customization Options

### Visual Settings

- **Line Width**: Adjust thickness of ADR levels

- **ADR Color/Style**: Customize appearance of ADR projection lines (solid, dashed, dotted)

- **Median Line**: Toggle visibility and customize appearance separately

- **Session Box Colors**: Customize each session's box color independently

- **Show Session Boxes**: Toggle session box visibility on/off

### Label Settings

- **ADR Labels**: Show/hide labels for ADR High and ADR Low, adjust size

- **Median Label**: Separate control for median line label

- **Session Labels**: Show/hide session name labels, adjust size

- **Label Colors**: Customize text colors for all labels

### Table Settings

- **Session Stats Table**: Position (9 locations available), size (Tiny to Huge), toggle on/off

- **Sample Sizes**: Show/hide the number of historical samples used for each calculation

- **Probabilities Table**: Separate position and size controls, toggle on/off

### Session Times

- Each session's time range can be customized to fit different markets or preferences

- All times are in Eastern Time (America/New_York timezone)

## Technical Notes

### Data Requirements

- The indicator requires sufficient historical data based on your lookback settings

- Minimum recommended: 50+ days of intraday data for reliable statistics

- Works on any timeframe below Daily (1-minute, 5-minute, 15-minute, etc.)

### Calculation Methodology

- **ADR Calculation**: Simple average of absolute daily high-low ranges

- **Session Statistics**: Mean average of ranges for each session filtered by day of week

- **Condition Detection**: Boolean logic comparing session high/low relationships

- All calculations update in real-time as new bars form

### Probability Data Source

The probability statistics displayed in the dynamic table are derived from:

- **Dataset**: 12 years of NQ (Nasdaq E-mini futures) historical data

- **Methodology**: Frequency analysis of outcomes following specific setup conditions

- **Time Period**: Multiple market cycles including various volatility regimes

**Critical Warning**: These probabilities are specific to NQ and reflect that instrument's behavior patterns. Market microstructure, participant behavior, and volatility characteristics differ significantly across instruments. Do not apply these NQ-derived probabilities to other markets (ES, RTY, YM, individual stocks, forex, commodities, etc.).

## Best Practices

1. **Combine with Other Analysis**: Use this indicator as one component of a complete trading methodology, not a standalone system

2. **Respect Risk Management**: Probabilities are not certainties; always use proper position sizing and stop losses

3. **Context Matters**: High-impact news events, holiday trading, and extreme volatility can invalidate typical patterns

4. **Verify Statistics**: Monitor your own results and compare to the displayed probabilities

5. **Adapt Session Times**: If trading instruments with different active hours, adjust session times accordingly

6. **Regular Calibration**: Periodically review if the session averages and probabilities remain relevant to current market conditions

## Understanding Originality

This indicator is original in its approach to combining three analytical frameworks into a single tool:

1. **Dynamic ADR Projection**: Unlike static pivot points, these levels adapt daily based on recent volatility

2. **Session-Specific Statistics**: Goes beyond simple volume profiles by quantifying average ranges for specific time windows across weekdays

3. **Conditional Probability Display**: Automatically detects overnight session relationships and displays relevant probability data rather than showing all scenarios simultaneously

The conditional logic system that determines which probability set to display is a key differentiator—traders only see the statistics relevant to the current market setup, reducing information overload and improving decision-making clarity.

## Summary

The **Statistical Daily Profile & Ranges** indicator provides traders with a comprehensive framework for understanding daily range potential, session-specific behavior patterns, and probability-based setup analysis. By combining ADR projection levels with detailed session statistics and dynamic probability displays, traders gain multiple perspectives on potential price movement within the trading day.

The indicator is most effective when used to:

- Set realistic profit targets based on average daily range

- Identify which sessions typically produce movement on specific weekdays

- Understand probability-weighted outcomes for different overnight setup conditions (NQ only)

- Visualize session ranges and compare them to historical averages

Remember that all statistical analysis reflects historical patterns, and market behavior can change. Always combine indicator signals with sound risk management, proper position sizing, and your own market analysis.

80% EDGE Rule - TPO Based═════════════════════════════════════════════════════════════

80% EDGE RULE - TPO BASED

═════════════════════════════════════════════════════════════

█ OVERVIEW

The 80% Edge Rule is a high-probability Market Profile concept that identifies when price is likely to traverse the prior session's Value Area. This indicator automates the detection, confirmation, and tracking of 80% EDGE Rule setups using true TPO (Time Price Opportunity) calculations—not volume profile.

When price opens outside the previous day's Value Area and then re-enters and is "accepted" back inside, there is an 80% statistical probability that price will travel to the opposite side of the Value Area. This indicator does all the heavy lifting: calculating the prior session's Value Area, detecting valid setups, confirming acceptance, and tracking progress toward the target.

█ THE 80% EDGE RULE EXPLAINED

The 80% Edge Rule is based on Market Profile theory developed by J. Peter Steidlmayer at the Chicago Board of Trade. The rule states:

❶ If price OPENS OUTSIDE the prior day's Value Area...

❷ And then ENTERS and is ACCEPTED back into the Value Area...

❸ There is an 80% chance price will rotate to the OTHER SIDE of the Value Area.

"Acceptance" is defined as price spending TWO OR MORE TPO periods (typically 30-minute blocks) inside the Value Area. This indicates that the market has accepted these prices as fair value, and the auction process will likely continue through to the opposite boundary.

BULLISH SETUP: Price opens BELOW the prior VAL → Enters and is accepted → Target is VAH

BEARISH SETUP: Price opens ABOVE the prior VAH → Enters and is accepted → Target is VAL

█ HOW THIS INDICATOR WORKS

This indicator performs several automated functions:

1. TPO VALUE AREA CALCULATION

• Analyzes the prior RTH (Regular Trading Hours) session

• Builds a true TPO distribution using 30-minute time blocks

• Each price level receives +1 TPO for each period it was touched

• Calculates POC (Point of Control) as the price with highest TPO count

• Expands from POC using the CME/CBOT standard "two-price" method until 70% of TPOs are captured

• This defines VAH (Value Area High) and VAL (Value Area Low)

2. SETUP DETECTION

• Monitors the RTH open (default 9:30 AM ET)

• Detects if price opened outside the prior Value Area

• Determines setup direction (Bullish or Bearish)

3. ACCEPTANCE MONITORING

• Tracks TPO blocks where price remains inside the Value Area

• Confirms setup when required number of blocks is reached (default: 2)

• Resets count if price exits VA before confirmation

4. TARGET & INVALIDATION TRACKING

• Monitors for target completion (opposite VA boundary)

• Monitors for invalidation (price moves beyond entry VA boundary + buffer)

• Visual feedback on outcome

█ VISUAL ELEMENTS

PRIOR VALUE AREA LINES (Dashed)

• RED DASHED LINE: Prior Day VAH (Value Area High)

• GREEN DASHED LINE: Prior Day VAL (Value Area Low)

• PURPLE DOTTED LINE: Prior Day POC (Point of Control)

TRADE LINES (Solid)

• YELLOW LINE: Entry price (where setup was confirmed)

• CYAN LINE: Target price (opposite VA boundary)

• GREEN LINE: Entry line turns green when target is hit

• GRAY LINES: Both lines turn gray if setup is invalidated

STATUS LABEL

• Floating label showing current setup state

• ORANGE "WATCHING": Setup detected, monitoring for acceptance

• YELLOW "CONFIRMED": Setup confirmed, tracking toward target

• GREEN "TARGET HIT ✓": Target successfully reached

• RED "INVALIDATED ✗": Setup failed, price moved against

DASHBOARD (Top Right Corner)

• Prior VAH: Yesterday's Value Area High

• Prior VAL: Yesterday's Value Area Low

• Prior POC: Yesterday's Point of Control

• Open Price: Today's RTH opening price

• Direction: BULLISH ↑ or BEARISH ↓

• Status: Current setup state

█ CONFIGURABLE SETTINGS

┌────────────────────────────────────────────────────────────

│ TPO SETTINGS

├────────────────────────────────────────────────────────────

│ Tick Size (Default: 0.25) │ • Price increment for TPO calculations

│ • ES/MES: 0.25

│ • NQ/MNQ: 0.25

│ • YM/MYM: 1.0

│ • RTY: 0.1 │ • CL/MCL: 0.01

│ • GC/MGC: 0.1

│

│ Value Area % (Default: 70)

│ • Percentage of TPOs to include in Value Area

│ • Standard is 70% (one standard deviation)

│ • Can adjust 50-90% based on preference

│

│ TPO Block Duration (Default: 30 minutes)

│ • Length of each TPO period

│ • Standard Market Profile uses 30-minute periods

│ • Adjust if using non-standard TPO settings

└────────────────────────────────────────────────────────────

┌────────────────────────────────────────────────────────────

│ 80% EDGE RULE SETTINGS

├────────────────────────────────────────────────────────────

│ TPO Blocks Required for Acceptance (Default: 2)

│ • Number of 30-min periods price must stay inside VA

│ • Standard rule requires 2 periods for acceptance

│ • More conservative: Increase to 3

│ • More aggressive: Reduce to 1 (not recommended)

│

│ Invalidation Distance (Default: 10 points)

│ • Buffer beyond VA boundary before setup is invalidated

│ • Bullish: Invalidates if LOW goes below VAL minus this distance

│ • Bearish: Invalidates if HIGH goes above VAH plus this distance

│ • Adjust based on product volatility and your risk tolerance

│

│ Fade Delay (Default: 5 minutes)

│ • How long entry/target lines stay visible after outcome

│ • Lines and floating label disappear after this delay

│ • Dashboard retains the outcome status until next session

└────────────────────────────────────────────────────────────

┌────────────────────────────────────────────────────────────

│ SESSION SETTINGS

├────────────────────────────────────────────────────────────

│ RTH Session (Default: 0930-1600)

│ • Regular Trading Hours window

│ • This determines which bars are used for TPO calculation

│ • Also determines when RTH "open" is detected

│

│ PRODUCT-SPECIFIC RTH SESSIONS:

│ • Equity Index Futures (ES, NQ, YM, RTY): 0930-1600

│ • Crude Oil (CL): 0900-1430 (pit session)

│ • Gold (GC): 0820-1330 (pit session)

│ • Treasury Bonds/Notes: 0720-1400

│ • Forex Futures: Varies by product

│

│ Timezone (Default: America/New_York)

│ • Timezone for session calculations

│ • Options: New York, Chicago, Los Angeles, UTC

│ • Use exchange timezone for accurate session detection

└────────────────────────────────────────────────────────────

┌────────────────────────────────────────────────────────────

│ VISUAL SETTINGS

├────────────────────────────────────────────────────────────

│ Show Prior VA Lines: Toggle VAH/VAL/POC lines on/off

│ Show Entry/Target Lines: Toggle trade-related lines on/off

│ VAH Color: Color for Value Area High line

│ VAL Color: Color for Value Area Low line

│ POC Color: Color for Point of Control line

│ Entry Line Color: Color for entry price line

│ Target Line Color: Color for target price line

│ Target Hit Color: Color when target is reached (default: green)

│ Line Width: Thickness of all lines (1-5)

└────────────────────────────────────────────────────────────

┌────────────────────────────────────────────────────────────

│ DEBUG SETTINGS

├────────────────────────────────────────────────────────────

│ Show Debug Info: Displays additional diagnostic information

│ • Session High/Low of prior day

│ • Current RTH status

│ • Current TPO block number

│ • Outcome timestamp

│ • Useful for troubleshooting or verifying calculations

└────────────────────────────────────────────────────────────

█ ALERTS

This indicator includes three configurable alerts:

① SETUP CONFIRMED

• Triggers when acceptance criteria is met

• Includes entry price and target price in alert message

② TARGET HIT

• Triggers when price reaches the opposite VA boundary

• Confirms successful completion of the 80% Rule setup

③ INVALIDATED

• Triggers when price moves beyond the invalidation threshold

• Signals that the setup has failed

To enable alerts:

1. Ensure "Enable Alerts" is checked in indicator settings

2. Right-click on the indicator → "Add Alert"

3. Select the condition you want to be alerted on

4. Configure notification method (popup, email, webhook, etc.)

█ RECOMMENDED USAGE

TIMEFRAME:

• Best used on 5-minute, 15-minute, or 30-minute charts

• The chart timeframe should divide evenly into 30 minutes

• Ensure sufficient historical bars are loaded for prior session calculation

BEST PRACTICES:

• Wait for full confirmation (2 TPO blocks inside VA) before considering entry

• Use the target line as your profit objective

• Consider the invalidation level for stop-loss placement

• Monitor the dashboard for real-time setup status

• Combine with other confluence factors (order flow, support/resistance, etc.)

IMPORTANT NOTES:

• This indicator calculates TRUE TPO-based Value Area, not volume profile

• Prior day VA is recalculated at each new session

• The 80% Rule is a statistical tendency, not a guarantee

• Always use proper risk management

█ ADJUSTING FOR DIFFERENT PRODUCTS

This indicator defaults to Equity Index Futures (ES, NQ, etc.) with:

• RTH Session: 0930-1600

• Timezone: America/New_York

• Tick Size: 0.25

FOR OTHER PRODUCTS, ADJUST:

CRUDE OIL (CL/MCL):

• RTH Session: 0900-1430

• Tick Size: 0.01

GOLD (GC/MGC):

• RTH Session: 0820-1330

• Tick Size: 0.10

TREASURY FUTURES (ZB, ZN):

• RTH Session: 0720-1400

• Tick Size: 0.03125 (ZB) or 0.015625 (ZN)

E-MINI DOW (YM/MYM):

• RTH Session: 0930-1600

• Tick Size: 1.0

RUSSELL 2000 (RTY):

• RTH Session: 0930-1600

• Tick Size: 0.10

Always verify the RTH session times and tick sizes for your specific product and exchange.

█ DISCLAIMER

This indicator is provided for educational and informational purposes only. It is not financial advice and should not be construed as a recommendation to buy or sell any financial instrument. Trading futures and other leveraged products involves substantial risk of loss and is not suitable for all investors.

Past performance is not indicative of future results. The 80% Edge Rule is a statistical observation based on Market Profile theory and does not guarantee any specific outcome. Always conduct your own analysis and use proper risk management.

Support and Resistance [Jamshid]📌 Support & Resistance

This indicator automatically identifies high-quality Support and Resistance zones using volume-weighted pivot levels. It visualizes price structure with adaptive volume boxes, breakout & retest signals, higher timeframe confirmation, and optional volume profile.

✅ Core Features

🔹 1. Smart Support & Resistance Zones (Volume-Based)

Detects pivot highs/lows with strong volume.

Boxes expand dynamically using ATR.

Zones display actual volume value.

Color intensity reflects volume strength.

🔹 2. Breakouts & Retests

“Break Sup / Break Res” labels on structure breaks.

Detects when old resistance becomes support (R→S).

Detects when old support becomes resistance (S→R).

Retest labels and diamond markers for holds.

🔹 3. Volume Profile (Optional)

Shows mini horizontal volume bars at each zone.

Separate bullish/bearish volume distribution.

Adjustable rows and lookback.

🔹 4. Higher Timeframe Confluence (Optional)

Check if current S/R aligns with HTF levels:

5m, 15m, 30m, 1H, 4H, Daily

Modes:

✅ Show All + HTF Labels

✅ Filter Only HTF Confirmed Levels

HTF confirmations shown directly on zone labels.

Tolerance setting for price matching.

🔹 5. Breaker Blocks (Failed S/R Reversal Zones)

Identifies bullish/bearish breaker zones.

Highlights breaker blocks on chart.

Optional labels and zone coloring.

🎯 Visual Alerts & Signals

✅ Breakouts (Support & Resistance)

✅ Retests (Hold without breakout)

✅ Role Reversal (R→S and S→R)

✅ Potential Bullish / Bearish Breakers

✅ Diamonds for hold/retest structure

✅ Labels with volume + timeframe confirmations

Every signal also has a built-in alertcondition so you can automate notifications.

⚙️ Customizable Settings

🟢 Main

Lookback period

Volume filter length

Box width multiplier

🎨 Visual

Show or hide labels, diamonds, retest labels

Label size

🟦 Breaker Blocks

Enable/disable breaker blocks

Show zones & labels

Custom colors

📊 Volume Profile

Enable/disable

Rows, lookback length

Bull/Bear color

⏳ Higher Timeframe Filtering

Turn HTF logic on/off

Select which timeframes to compare

Filter mode or label mode

Price matching tolerance (%)

✅ Why this indicator is unique

✔ Combines price structure + volume + HTF confluence

✔ Automatically adapts S/R strength using volume data

✔ Shows role reversal and breaker logic

✔ Smart visual alerts & automation support

✔ Highly customizable for any strategy or timeframe

💡 How to Use

Add the indicator to any chart or timeframe.

Look for high-volume S/R zones (darker colors = stronger).

Watch for:

Breakouts (trend continuation or reversal)

Retests (strong confirmations)

HTF confluence (higher probability)

Breaker blocks (failed level reversal)

Optionally enable alerts for automation or notifications.

******************************************************************

⚠️ Dangers of Trading

1️⃣ You can lose money very fast

Markets move quickly, and leverage makes losses even faster. Even experienced traders go through drawdowns.

2️⃣ Emotional decisions ruin accounts

Fear (selling too early) and greed (holding too long or overtrading) cause most losses. Trading is more psychological than technical.

3️⃣ Overconfidence after small wins

Many traders win at the beginning and believe they “mastered” the market, then take big risks and blow the account.

4️⃣ No system = gambling

If you trade without clear rules and risk management, you’re not trading—you’re gambling.

5️⃣ Market is not fair

Smart money, institutions, HFT algorithms, and stop-hunts exist. Retail traders are often the liquidity for bigger players.

6️⃣ News/Unexpected events

Unpredictable events (CPI, FOMC, war, tweets, etc.) can instantly move the market against your position.

✅ Advice for Safer & Smarter Trading

✅ 1. Protect your capital first

Your number one job is to survive.

Never risk more than 1–2% per trade.

✅ 2. Have a written trading plan

Define:

When to enter

When to exit

How much to risk

What conditions must be present

If your plan is not written, you don’t have a plan.

✅ 3. Use Stop Loss always

No stop loss = account suicide.

Even professional traders are wrong sometimes.

✅ 4. Focus on one strategy (mastery > trying everything)

Jumping from one strategy to another causes confusion. One good strategy with discipline beats five strategies with no consistency.

✅ 5. Trade with the trend and higher timeframe direction

Trading against HTF structure is fighting the market.

✅ 6. Control emotions like a machine

Biggest trader enemies:

Overtrading

Revenge trading

Fear of missing out (FOMO)

When emotions are strong → stop trading.

✅ 7. Be patient (best skill of a trader)

Sometimes the best trade is no trade.

Professional traders wait for high-probability setups.

✅ 8. Backtest and demo before using real money

If it doesn’t make money in backtesting or demo, it won’t magically work live.

✅ 9. Accept losses (they are part of the game)

Even the best traders lose. The key is small losses, big wins.

✅ 10. Keep learning forever

Market changes. What works today may not work tomorrow. Study price action, volume, psychology, risk management.

🧠 Final Truths:

✅ Trading is a business, not easy money

✅ Winning rate doesn’t matter—risk/reward matters

✅ Consistency > luck

✅ Discipline > knowledge

✅ Survival > profit